On 30 August 2019, the Institute had the opportunity to present our submission on the Climate change Response (Zero Carbon) Amendment Bill in front of the Select Committee at Parliament. The Select Committee consisted of MPs Angie Warren-Clark (Labour Party), Jenny Marcroft (NZ First Party), Ian McKelvie (National Party), and Stuart Smith (National Party).

The introduction of the Climate Change Response (Zero Carbon) Amendment Bill represents a significant development in New Zealand’s climate change discourse, which has historically centred on the New Zealand Emissions Trading Scheme (NZ ETS) as the primary policy mechanism for reducing emissions. The Bill will embed the 1.5° C target of the Paris Agreement in New Zealand legislation, establishing ‘a framework by which New Zealand can develop and implement clear and stable climate change policies’. Current and future climate change discourse in New Zealand is likely to centre on transitioning to a low-carbon economy, as well as the target of reaching net-zero emissions in New Zealand by 2050.

Between June and July 2018, the Bill was open for consultation for the public, resulting in over 15,000 submissions. Over the last few months it has been introduced into the House of Representatives and is currently under consideration by the Select Committee.

Isabella Smith, Wendy McGuinness (CEO), and Reuben Brady at the Select Committee hearing.

The Institute’s submission was supported by additional material now published as McGuinness Institute Oral Submission: Climate Change Response (Zero Carbon) Amendment Bill; as well as Think Piece 32 – Exploring Ways to Embed Climate Reporting in the Existing Framework, which was prepared specifically for the hearing and is now published here. As an extension to the submission, the think piece outlined any further points of interest, areas for improvement and thoughts on amendments to the Bill. The think piece is centred around a diagram that maps out the existing reporting framework in terms of relevant international organisations and pronouncements and legislation, and the New Zealand framework and legislation. Policy levers that could be used to embed climate reporting requirements into the existing framework are indicated with a numbered key that corresponds to the relevant parts of the framework.

Wendy McGuinness presented the Institute’s submission, which was broken down into three sections.

1. Key observations:

- We fully support the purpose of the Bill, which is to ‘provide a framework by which New Zealand can develop and implement clear and stable climate change policies that contribute to the global effort under the Paris Agreement to limit the global average temperature increase to 1.5° Celsius above pre-industrial levels’ (Explanatory note).

- The Bill contains three essential components: institutions (i.e. Climate Change Commission), instruments (i.e. emission budgets, risk assessment and adaptation plan) and information (i.e. provision of information).

- The Bill contains three essential processes: risk identification (i.e. the risk assessment), measurement (i.e. emissions and emission budgets) and management (i.e. the adaptation plan).

2. Key observations regarding information

Table 1: High level analysis of information requirements mentioned in the Bill

| Key characteristics | Bill | Outstanding issues |

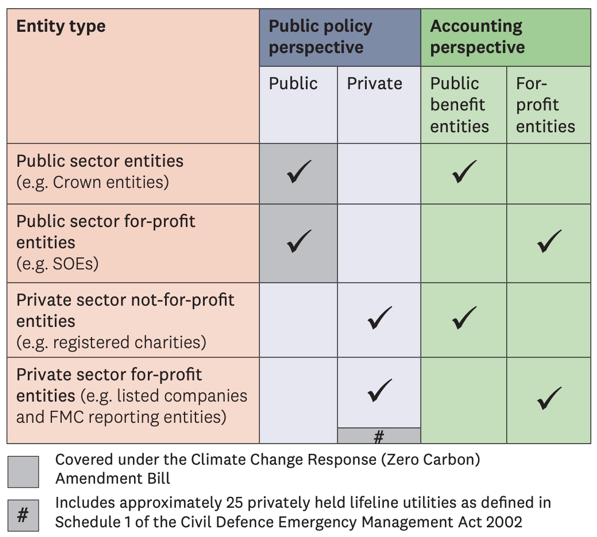

| 1. Who | Public sector entities and some privately held lifeline utilities (see figure below) |

Other private sector and industry organisations should also be included. Note: s 5ZW(1)(a) refers to ‘different sectors’ (which implies primary/secondary sectors). See 3.1 and 3.2 below. |

| 2. What | Listed in s 5ZV(1) |

‘Provision of Information’ to be separated in a new Part 1D and emissions to be included in list (as necessary for preparing and tracking budgets). See 3.3 and 3.4 below. |

| 3. When | At discretion of Minister (via regulations) | No issues. |

| 4. Where (where information is made available to the public) |

Delivered from Minister to the Commission |

Clarity required that information provided to the Commission will be publicly available and the Commission will be responsible for creating a repository over time. Note: s 5B does not discuss role of being a repository or providing public access to information. See 3.5 below. |

| 5. How (how information is prepared, sought and delivered) |

To be outlined in regulations |

Suggest alignment with existing reporting frameworks added to list in s 5ZW(2) – a new (d). See 3.6 below. |

3. Areas of concern and suggested solutions

3.1 Private sector and industry organisations should be included under new ss 5ZV(4)(j)–(m).

Suggestion:

- Add the following entities to the list in s 5ZV(4):

(j) listed companies,

(k) large companies (as defined in s 45 of the Financial Reporting Act 2013),

(l) FMC reporting entities, and

(m) other selected entities as considered appropriate.

3.2 More clarity is required over the existing list of reporting organisations under s 5ZV(4).

Suggestions:

- Amend s 5ZV(4)(e) to read ‘non-listed companies in which the Crown is a majority or sole shareholder listed in Schedule 4A of the Public Finance Act 1989’.

- Amend s 5ZV(4)(f) to read ‘state enterprises listed in Schedule 4A of the Public Finance Act 1989’.

3.3 Sections under ‘Power to request provision of information’ should include emissions and be treated as a separate, new Part 1D.

Suggestions:

- Make the sections in Part 1C under ‘Power to request provision of information’ into a separate, new Part 1D.

- Rename s 5ZV ‘Minister may require certain organisations to provide information on climate change adaptation’ to s 5ZV ‘Minister may require certain organisations to provide information on how the organisation impacts the climate and how the climate impacts the organisation.’

3.4 Include carbon accounting and assurance information (under s 5ZV (1) (a)).

Suggestion:

- Amend s 5ZV(1)(a) to include carbon emissions accounting and, where appropriate, assurance as part of the ‘metrics and costs used to understand and benchmark the effects of climate change’.

3.5 Consider providing more clarity over the role the Commission has in being a repository of climate change over time (under 5B).

Suggestion:

- Add a new s 5B(c) to include a purpose of the Commission ‘to be a repository of climate-related information collected by or provided to the Commission and to ensure that public information is made publicly available in a timely manner’.

3.6 Consider accounting for alignment with existing reporting frameworks as part of s 5ZW(2).

Suggestion:

- Add a new s 5ZW(2)(d) ‘the alignment of new reporting frameworks with existing reporting frameworks’.

Background

This year, the Institute’s work has been shaped by the alarming state of climate reporting within New Zealand. A number of publications have been pivotal for drawing our conclusions:

- Working Paper 2018/03 – Analysis of Climate Reporting in the Public and Private Sectors

- Discussion Paper 2019/01 – The Climate Reporting Emergency: A New Zealand case study

- Working Paper 2019/04 – Analysis of Government Department Strategies Between 1 July 1994 and 31 December 2018

- Working Paper 2019/05 – Reviewing Voluntary Reporting Frameworks Mentioned in 2017 and 2018 Annual Reports

- Working Paper 2019/06 – Update: Analysis of Climate Change Reporting in the Public and Private Sectors

In terms of climate-related disclosures in New Zealand, there is a significant gap between what users want and what preparers provide. This gap is due to a lack of a structural response to a complex and critical issue facing existing and future generations. The International Accounting Standards Board (IASB), an independent international standard-setter, was designed to respond to financial reporting issues that are generally backward-looking, and when forward-looking, only report risks with a high level of certainty. This means it is not well suited to address the risks of climate change with consistent and mandatory reporting standards, which has resulted in a multiplicity of voluntary reporting frameworks emerging internationally. Many of the voluntary frameworks attempt to address the same issues, saturating the market and producing siloed and diluted results.

This poses a significant challenges for businesses and countries that wish to improve their climate reporting. Long-term strategies to mitigate and adapt to climate change are required to make businesses and countries more socially just, environmentally robust and economically durable.

Next steps

- Report 17 – ReportingNZ: Building a Reporting Framework Fit for Purpose. This Project 2058 report aims to lay groundwork for a review of New Zealand’s reporting framework. Such a review would have the end goal of improving New Zealand’s information infrastructure, making it fit for purpose for both users and preparers by making information (especially climate-related information) useful, accessible, accurate, timely, cost-effective and comparable.

- Working Paper 2019/07 – A Review of the Accounting and Assurance of Greenhouse Gas Emissions. This working paper attempts to answer a series of questions about emissions reporting as they relate to a range of international climate reporting regimes:

1. Who should report?

2. Where should this information be disclosed?

3. What methodologies should be used?

4. What GHG Protocol scopes (1–3) should be reported?

5. Should emission disclosures be assured? - Help facilitate implementation of the Recommendations of the TCFD. This may include a workshop for entities on how to apply the Recommendations of the TCFD.

- Explore the idea of a New Zealand Green Finance Strategy. This would be along the lines of the UK Green Finance Strategy discussed in more detail in Section 7.5 of Discussion Paper 2019/01 – The Climate Reporting Emergency: A New Zealand case study.