Report 17 – ReportingNZ: Building a Reporting Framework Fit for Purpose is a major publication from policy Project ReportingNZ, which aims to contribute to a discussion on how to build an informed Aotearoa New Zealand. The report reviews New Zealand’s external reporting framework and assesses whether it is fit for purpose, then suggests a series of recommendations on what actions could be undertaken to ensure the reporting framework provides the necessary information directors, investors, bankers and other stakeholders require to make effective and timely decisions.

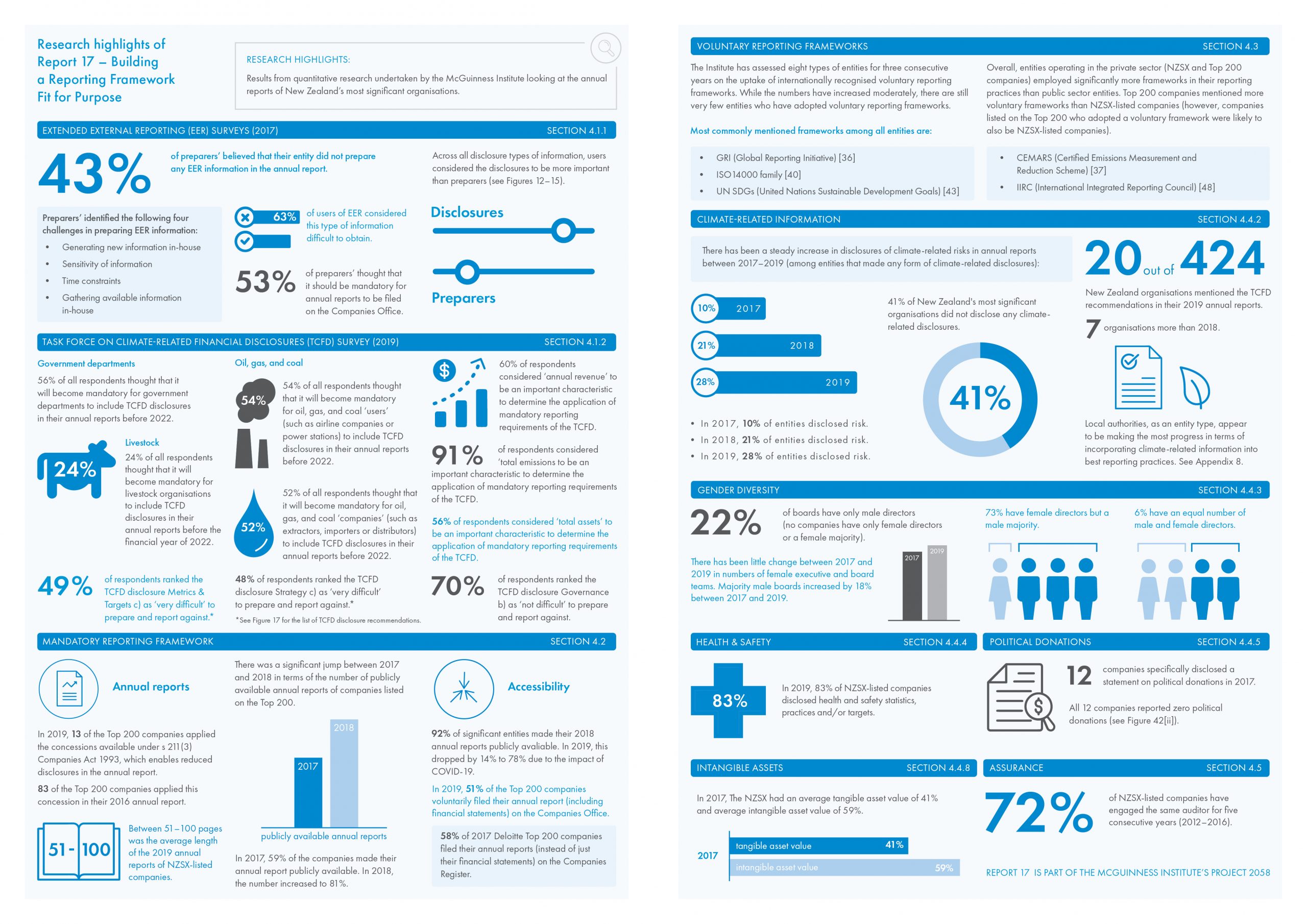

Report 17 brings together over three years of the McGuinness Institute’s research and analysis of the New Zealand reporting framework – the country’s information infrastructure. See some of the key research highlights below (they can also be found on pp. 39–40 of Report 17.).

In the report’s Foreword, Professor Ian Ball makes the following observation:

The lesson is that reporting has real world consequences. It creates understanding and motivates action. It shapes decisions and outcomes. It impacts our wellbeing. This is true in the corporate sector, the public sector, and for charities. – Professor Ian Ball

It is just over 30 years since the Public Finance Act 1989 was enacted and almost 30 years since the Companies Act 1993 was passed. It is timely to ensure New Zealand’s reporting framework is fit for purpose. Like any piece of public good infrastructure, the external reporting framework deserves attention and investment.

Report 17’s aim is threefold. Firstly, to provide an overview of the Institute’s research findings and analysis to date, evidencing what is working and not working within the current system. Secondly, to provide observations and recommendations for policy-makers and other interested parties on how the current system can be improved. In undertaking this research, the Institute found that the current reporting framework is outdated, stagnant, inflexible and, arguably, costly. In its present state, the reporting framework is unlikely to be responsive to the future needs of shareholders and other stakeholders. The third and final aim is to lay the groundwork for a comprehensive review of New Zealand’s reporting framework.

Report 17 is part of a series of reports that aim to contribute to the type of infrastructure New Zealand will need to improve wellbeing and generate sustainable growth over the long term. These reports come under the Institute’s flagship Project 2058. Find Report 17 and other Project 2058 reports here.

Launch

The report was launched on Thursday, 18 June 2020 at a lunchtime presentation attended by policy experts from a range of institutions. Launch attendees (or those briefed shortly afterwards) included MBIE, MfE, XRB, Treasury, IoD, NZX, FMA, OAG, RBNZ and CA ANZ.

Wendy McGuinness began the presentation by reflecting on the three eras of the reporting framework since 1970, identifying its associated trends and implications, and illustrating issues and weaknesses with the current reporting framework. The presentation then loosely followed the structure of the report itself, paired with the slides below. The presentation led to an open and engaging roundtable discussion.

Key Finding

The most significant finding derived from the conclusions made in Legal Opinion 2020/01 – Obligations on directors to report risk in New Zealand annual reports under the Companies Act 1993 (May 2020), found here. The opinion found that although directors of New Zealand entities are obliged to take climate-related financial risks into account, there is no obligation for directors to report on those risks in an entity’s annual report. This means directors in New Zealand are not obliged to inform shareholders about climate risks (or indeed any other risks) in their annual reports.

This finding represents a significant information gap for shareholders and broader stakeholders that must be rectified. This finding is both urgent and important given the significant risks, some of which are systemic, that the climate and COVID-19 crises are creating.

Fortunately, the skills required to report against TCFD, can also be applied to COVID-19 (e.g. the resilience of an organisation’s strategy when it takes into account different scenarios and the identification, assessment and management of risk). The pandemic has made it even more important to introduce mandatory reporting against TCFD, so that we can have an informed market that drives investment, innovation and public policy in a direction that is durable, certain and sustainable.

Overview of Major Recommendations

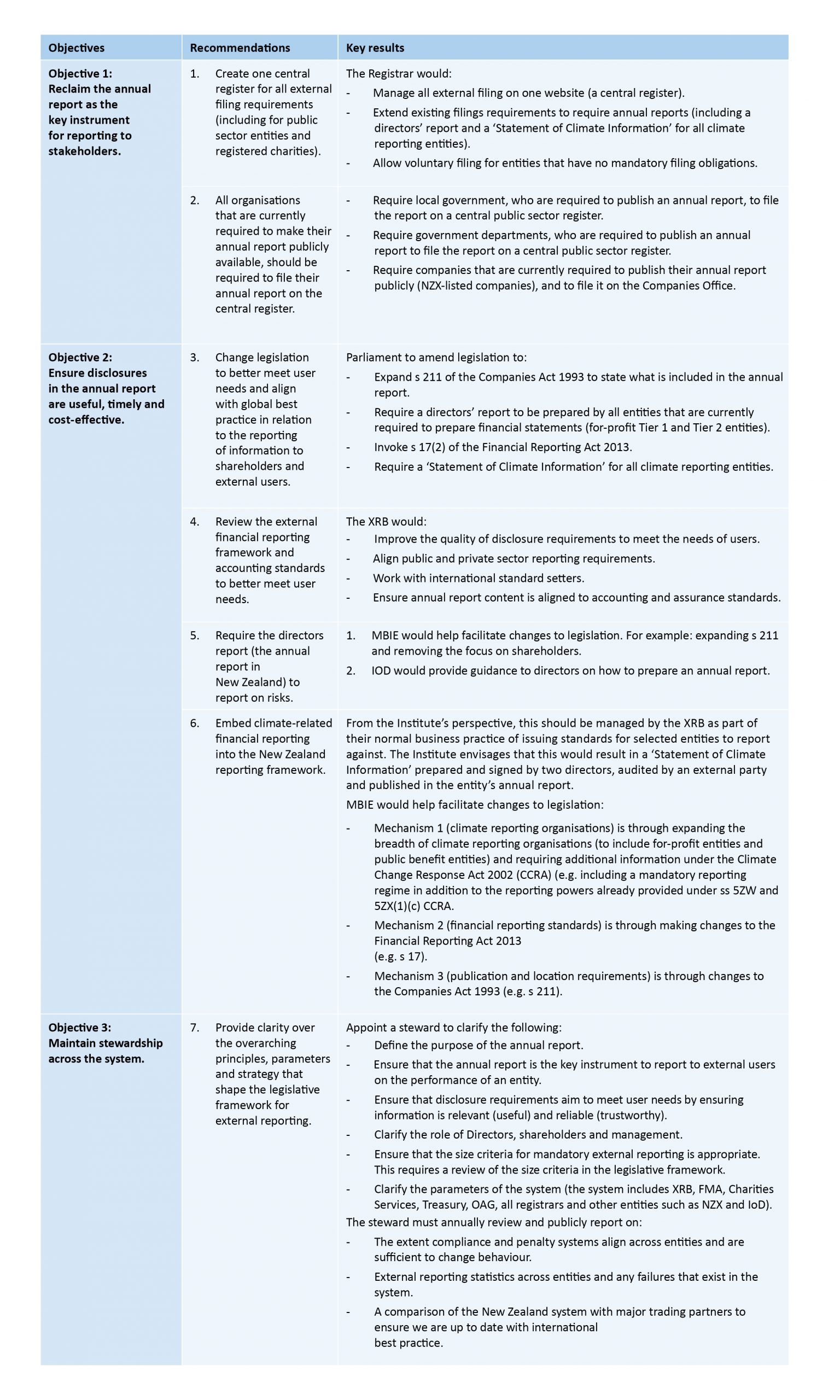

Section 8 of the report outlines the seven major recommendations, summarised in the table below (see pp. 136–137 of Report 17). The recommendations set out the actions the Institute believes New Zealand should implement. Some are low-hanging fruit (e.g. not expensive to implement and require minimal change/s to legislation) whereas others will require further analysis and dialogue with other key players before consultation and ideally legislative change.

Acknowledgements

The Institute would like to thank the staff from key institutions who helped inform our understanding of the reporting framework. Without their interest and support, this report would not have been possible.

In particular, we would like to thank Andrew Tait, Dr Ramona Zharfpeykan, Gillian McIlraith, Karen McWilliams and Zowie Pateman for providing specific technical feedback in response to our invitation to comment on the draft report. We would also like to thank Geoff Connor, for sharing his time, technical expertise and strategic knowledge. We would like to acknowledge the support of Fitzgerald Strategic Legal, BDO (Wellington), Kensington Swan (Wellington), Simpson Grierson (Auckland) and the External Reporting Board (XRB), who answered our questions and ensured that our application of legislation and the accounting standards framework throughout the report is accurate. This report could not have been completed without the expertise and passion of Lay Wee Ng, she was a delight to work with as we navigated the intricacies of the reporting framework. However, any errors remain our responsibility.

This report has been built on the knowledge and experiences of a wide range of people; it has been invaluable to learn and share the observations of report users and preparers. To all of you: thank you for challenging our thinking and sharing your wisdom.

Finally, Wendy would also like to thank the patience and the passion of the McGuinness Institute team that brought this work to a close.

Contact us

Please do not hesitate to contact Wendy at the Institute if you would like to meet to discuss the recommendations in more detail.

Background

The Institute placed Report 17 on hold in 2019 in order to publish Discussion Paper 2019/01 – The Climate Reporting Emergency: A New Zealand case study. This paper had a specific focus on climate-related reporting, as the Institute considered this a significant and urgent area to address given events that unfolded in 2019, namely the passing of the 2019 Climate Change Response (Zero Carbon) Amendment Bill and reforms to the NZ ETS. The paper was published in October 2019 and is available here.

Selected ReportingNZ publications since 2011

The full list of publications can be found in Appendix 1 of Report 17.

Integrated Annual Report Survey of New Zealand’s Top 200 Companies: Exploring Responses from Chief Financial Officers on Emerging Reporting Issues (January 2011)

Preparers’ Survey: Attitudes of the CFOs of significant companies towards Extended External Reporting (published in collaboration with the XRB) (10 April–3 July 2017)

Users’ Survey: Attitudes of interested parties towards Extended External Reporting (29 May–21 August 2017)

Survey Insights: An analysis of the 2017 Extended External Reporting Surveys (March 2018)

Survey Highlights: A summary of the 2017 Extended External Reporting Surveys (March 2018)

ReportingNZ Overview Worksheet: An analysis of the state of play of Extended External Reporting (March 2018)

Working Paper 2018/01 – NZSX-listed Company Tables (March 2018)

Working Paper 2018/03 – Analysis of Climate Change Reporting in the Public and Private Sectors (July 2018)

Working Paper 2018/04 – Legislation Shaping the Reporting Framework: A compilation (September 2018)

Think Piece 30 – Package of Climate Change Reporting Recommendations (October 2018)

Submission to Ministry for the Environment on the Climate Change Response (Zero Carbon) Amendment Bill (July 2019)

Oral Submission to Select Committee on Climate Change Response (Zero Carbon) Amendment Bill (August 2019)

Working paper 2019/05 – Reviewing Voluntary Reporting Frameworks Mentioned in 2017 and 2018 annual reports (September 2019)

Working Paper 2019/06 – Updated Analysis of Climate Change Reporting in the Public and Private Sectors (September 2019)

Think Piece 32 – Exploring Ways to Embed Climate Reporting in the Existing Framework (September 2019)

Discussion Paper 2019/01 – The Climate Reporting Emergency: A New Zealand case study (October 2019)

Survey Insights: An analysis of the 2019 Task Force on Climate-related Financial Disclosures (TCFD) survey (December 2019)

Submission on Climate-related financial disclosures: Understanding your business risks and opportunities related to climate change (December 2019)

Legal Opinion 2020/01 – Obligations on directors to report risk in New Zealand annual reports under the Companies Act 1993 (May 2020)

Working Paper 2020/02 – The Role of a Directors’ Report: An analysis of the legislative requirements of selected Commonwealth countries (May 2020)

Working Paper 2020/03 – Reporting Requirements of Five Types of Entities (June 2020)

Working Paper 2020/04 – Analysis of Climate Reporting in the Public and Private Sectors (June 2020)

Working Paper 2020/05 – Reviewing Voluntary Reporting Frameworks mentioned in 2019 Annual Reports (June 2020)

About Project 2058

Project 2058 is informed by three policy projects and seven research projects. Report 17 sits under the Institute’s policy project ReportingNZ, and is the first in a series of three. The other two reports will explore additional aspects of policy, namely New Zealand’s strategy framework (StrategyNZ) and New Zealand’s foresight framework (ForesightNZ). The underlying assumption of these reports is that reporting informs foresight, foresight shapes strategy and strategy requires reporting. If all three capabilities are aligned and given equal weight, then the system should deliver durable outcomes for all New Zealanders. Equally, if New Zealand has the skills to develop good strategy and the ability to obtain quality foresight but fails to report against strategy or report on changes in foresight, New Zealand will not know if it is moving in the right direction.

Project 2058 is the Institute’s flagship project and is used to drive our focus on New Zealand’s long-term future to the year 2058. The year 2058 was selected in 2008 as a year distant enough in the future to avoid self-interest but close enough to realistically drive the Institute’s work programme.